-

Basic bot/template for managing multiple positions and single order per position with stoploss and take profit

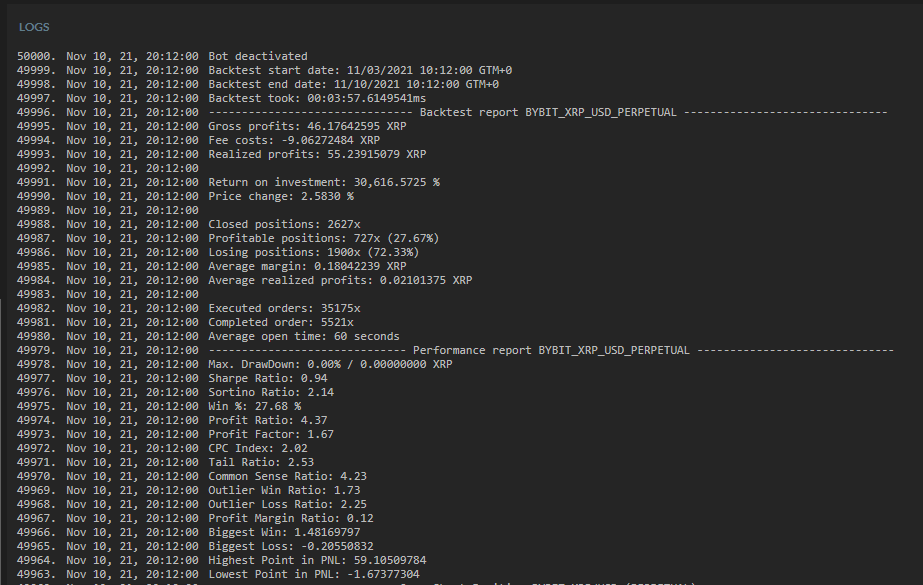

Get a signal from where ever you like either from another script or remote signal and it will manage multiple positions both long and short.

Requires my other custom commands to work –

[cmd] GetPID (getPositionId)

[cmd] getOID

[cmd] CheckOpenOrder

[cmd]CheckPositionId— Author – Strooth – Find me on discord – strooth#4739

— Feel free to donate to support my work or if my script helped you in any way <3

— BTC Adress: 33MsEAbA8tg7SpohgnCpSrmPTBih2UkhxQ

—-

This topic was modified 2 years, 4 months ago by

.

.

-

This topic was modified 2 years, 4 months ago by .

-

This topic was modified 2 years, 4 months ago by .

-

This topic was modified 2 years, 1 month ago by

.

.

-

This topic was modified 1 year, 10 months ago by .

-

This topic was modified 1 year, 3 months ago by .

-

This topic was modified 1 year, 3 months ago by .

-

This topic was modified 2 years, 4 months ago by