-

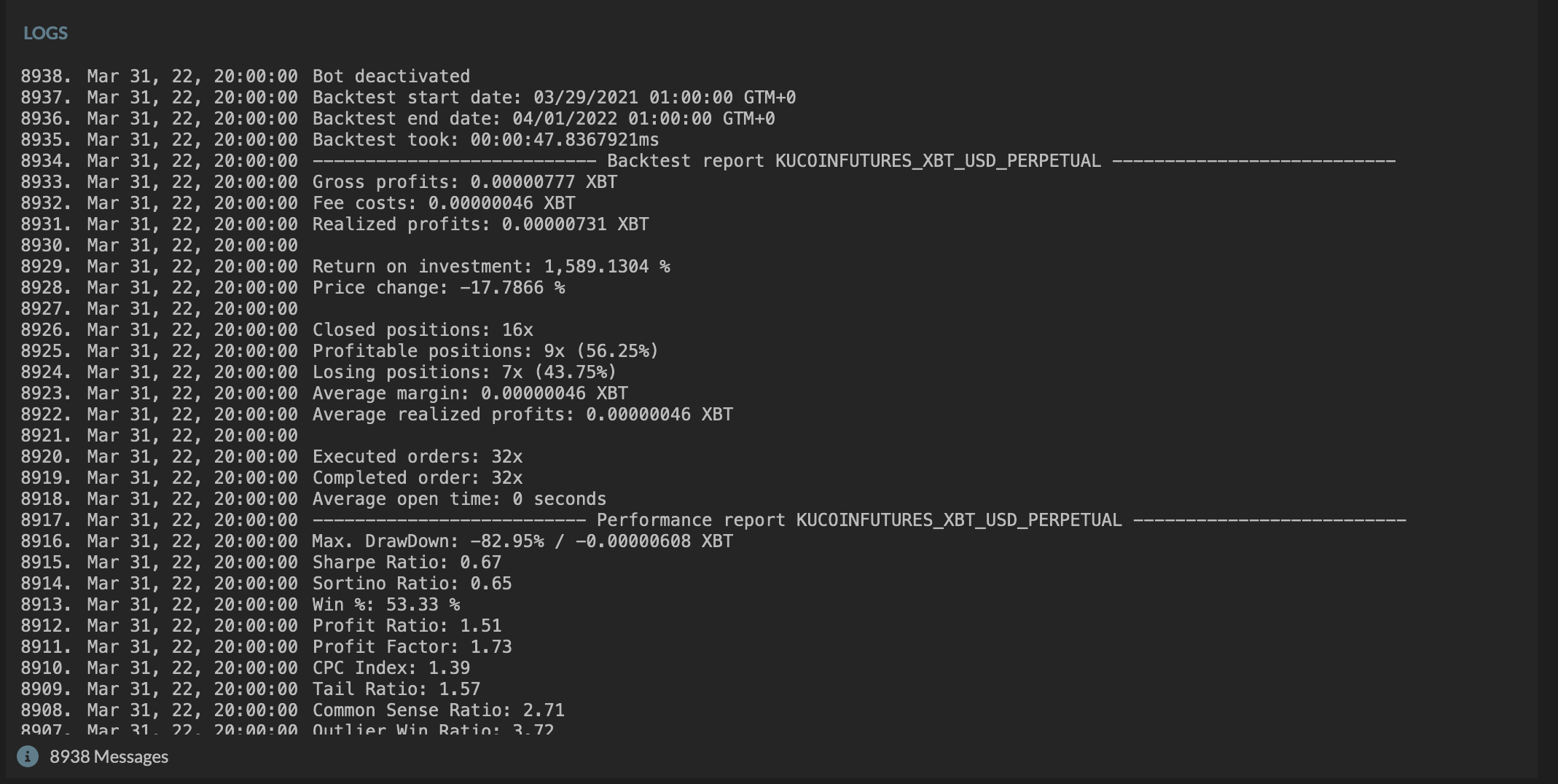

This is a short only strategy that does really well on large time frames.

The defaults work well on BTC_USD on the 1 hour time frame.

Its important to note on a 1 year backtest only about 16 trades occur. Meaning that this bots orders are statistically insignificant but feel free to try it out.

-

This topic was modified 2 years ago by

r4stl1n.

Related Scripts From This Author

-

This topic was modified 2 years ago by

-

-

May 21, 2022 at 3:09 PM #3030

romdisc

Basic::This is much more cleaner:

`lua

— [r4stl1n] Triple VWAP Trend Rider

—

— This strategy utilizes the VWAP_Window function to

— execute shorts when conditions are meet——————————–

— You are on your own with this script

——————————–

— ~Bored and programming~HideOrderSettings()

— Wrap our entire strategy in the OptimizedForInteral

— To ensure our strat only runs on new complete candles

rsiLength = Input (“RSI Length”, 60,””)

rsiShortLevel = Input(“RSI Short”,30,”RSI Short Level”,””)ppoShort = Input(“POI Short”,9,”POI Short Level”,””)

ppoLong = Input(“POI Long”,26,”POI Long Level”,””)

ppoSignal = Input(“POI Signal”,-1,”POI Signal”,””)vwapWindowOne = Input(“VWAP Window One”,20,”VWAP Window Size”,”VWAP Settings”)

vwapWindowTwo = Input(“VWAP Window Two”,60,”VWAP Window Size”,”VWAP Settings”)

vwapWindowThree = Input(“VWAP Window Three”,250,”VWAP Window Size”,”VWAP Settings”)— First we grab a day candles

OptimizedForInterval(0, function()local vwap20 = CC_VWAPWindow(vwapWindowOne)

local vwap60 = CC_VWAPWindow(vwapWindowTwo)

local vwap250 = CC_VWAPWindow(vwapWindowThree)local rsi = RSI(ClosePrices(),rsiLength)

local ppo = PPO(ClosePrices(),ppoShort,ppoLong,EmaType)if vwap250[3] != nil

and CurrentPrice().close < vwap250[1] and GetPositionDirection() != PositionShort

and vwap20[1] < vwap60[1]

and vwap60[1] < vwap250[1]

and ppo[1] <= ppoSignal

and rsi > rsiShortLevel

and vwap250[1] < vwap250[12]

then

PlaceGoShortOrder(0,TradeAmount(), {type=MarketOrderType, note=’S’})

endif GetPositionDirection() == PositionShort

and vwap60[1] >= vwap250[1]

PlaceExitShortOrder(0,TradeAmount(), {type=MarketOrderType, note=’E’})

endPlot(0, “vwap20”, vwap20, {c=Cyan})

Plot(0, “vwap60”, vwap60, {c=Red})

Plot(0, “vwap250”, vwap250, {c=Green})Plot(1, “RSI Level”,rsi)

Plot(2, “PPO Level”,ppo)end)

` -

June 3, 2022 at 7:20 PM #3078

KobaltBasic::

KobaltBasic::Cool Looking at above trades [if the first position was kept vs exits, re-entry]

Are you [like me] also still are tackling the same hurdle:

How to NOT close your Short [only reduce to a minimum 1x leverage cross] until bullish confirmation (increase BTC and hedge its USD] or have a re entry mechanism SL for the minimum portion of your accounts equity?

Have closed it too often and was ‘naked’ ‘long unnecessary . very deja vu isn’t it? ;p-

June 3, 2022 at 7:30 PM #3079KobaltBasic::

Arguably both are just as clean

I think this for me gives a clear view of what you would achieve with IfElseIf chains in VE and especially the levels you need to end :—

”’ if CurrentPrice().close < vwap250[1] and GetPositionDirection() != PositionShort

then

if vwap20[1] < vwap60[1]

then

if vwap20[1] < vwap250[1]

then

if vwap60[1] < vwap250[1]

then

if ppo[1] <= ppoSignal

then

if rsi > rsiShortLevel

then

if vwap250[1] < vwap250[12]

then

PlaceGoShortOrder(0,TradeAmount(), {type=MarketOrderType, note=’S’})

end

end

end

end

end

end

end

end”’-

This reply was modified 1 year, 11 months ago by

Kobalt.

Kobalt.

-

This reply was modified 1 year, 11 months ago by

-

-